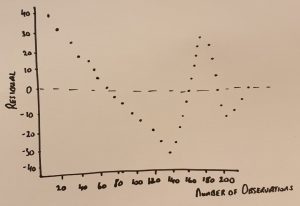

In econometrics, a fantastic way of observing the relationship between the respective error observations within a given data set is through a visual relationship. It makes any relationship immediately obvious when you draw a representation of the residual level present within the data set.

What we see here is what can be described as a cyclical pattern in the dataset where the residual both rises and falls together. In this case, there is a direct correlation between the residuals represented in this econometric data set. The reason being is that as one error term is positive and is rising upwards, it appears to make it more likely that the following observation of error will rise also therefore there is a correlation between the two.

The opposite case is also seen as where the observation of the residual is seen to be falling then we see that the observation which follows is more likely to be falling also. As a result of this there is a pattern emerging. This is a cyclical pattern and as a result, in Econometrics, we would state that there is clearly a correlation between the observations of the error terms and therefore Classical Assumption 4 has been violated.

Always remember that throughout your studies and examinations in econometrics, that the error term should always be random. If any pattern is visible, you have a correlation issue and the integrity of the model has been compromised.

Find us on facebook:

https://www.facebook.com/corkschoolofeconomics

Check out our World-Class Econometrics courses here: