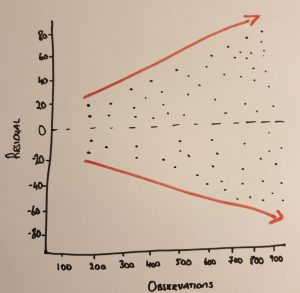

In econometrics, variance can be described as the spread of the data from the average value of the data set in question. When running Ordinary Least Squares (OLS), it is vital that this level of variation in the data stays constant. If the variance of the errors in the data set is not consistent but instead begins to rise, your data is exhibiting what is referred to as Heteroskedasticity. As seen by the red arrows the diagram below, this is where the variance or spread of the residual increases as more and more observations are included in the model.

Think of this scenario: Can you imagine being hired by a financial firm to run econometric analysis using an Ordinary Least Squares (OLS) Linear Regression across all of their investments? When you are midway through the process, the financial board asks you how you are progressing and you say that it is going well but the spread of error (Variance) is increasing as you introduce more financial observations. This would spell big trouble. As a consequence, the accuracy of your estimates in this Ordinary Least Squares (OLS) Linear regression would be compromised.

Find us on facebook:

https://www.facebook.com/corkschoolofeconomics

Check out our World-Class Econometrics courses here: